The backg round to ‘The Alternative Remedies Package’ is well documented, in fact it could justify a book. After ‘Humpty fell off the Wall’ in 2008 and RBS had to be recapitalized by the UK Government to the tune of £45 billion, the European Commission ruled this was a form of ‘State Support’ and because RBS already had a high market share in the SME banking market, a package of ‘penalities’ was imposed to reduce their ‘unfair advantage’.

round to ‘The Alternative Remedies Package’ is well documented, in fact it could justify a book. After ‘Humpty fell off the Wall’ in 2008 and RBS had to be recapitalized by the UK Government to the tune of £45 billion, the European Commission ruled this was a form of ‘State Support’ and because RBS already had a high market share in the SME banking market, a package of ‘penalities’ was imposed to reduce their ‘unfair advantage’.

Initially they were instructed to ‘divest themselves’ of a large number of SME accounts. The decision was made to physically hive off a large number of SME accounts, and the bank staff that dealt with them, into a dormant bank they owned, Williams & Glyn. The first hurdle was renewing its banking licence (the banking equivalent of letting the MOT run out on your car). The second hurdle was attracting buyers for the resultant business, and the final straw was the inability to ‘decouple’ the IT system for this part of the bank, which killed any possible sale.

RBS then had no option but to agree to an imposed alternative – ‘The Alternative Remedies Package’.

This has two components:

A £425m ‘Capability and Innovation Fund’ which involves RBS having to ‘donate’ this sum for selected eligible organisations to develop their capabilities to compete in the business banking market. Eligible organizations include challenger banks and so called ‘Fintech’ companies, developing business banking under the new ‘Open Banking’ regulations.

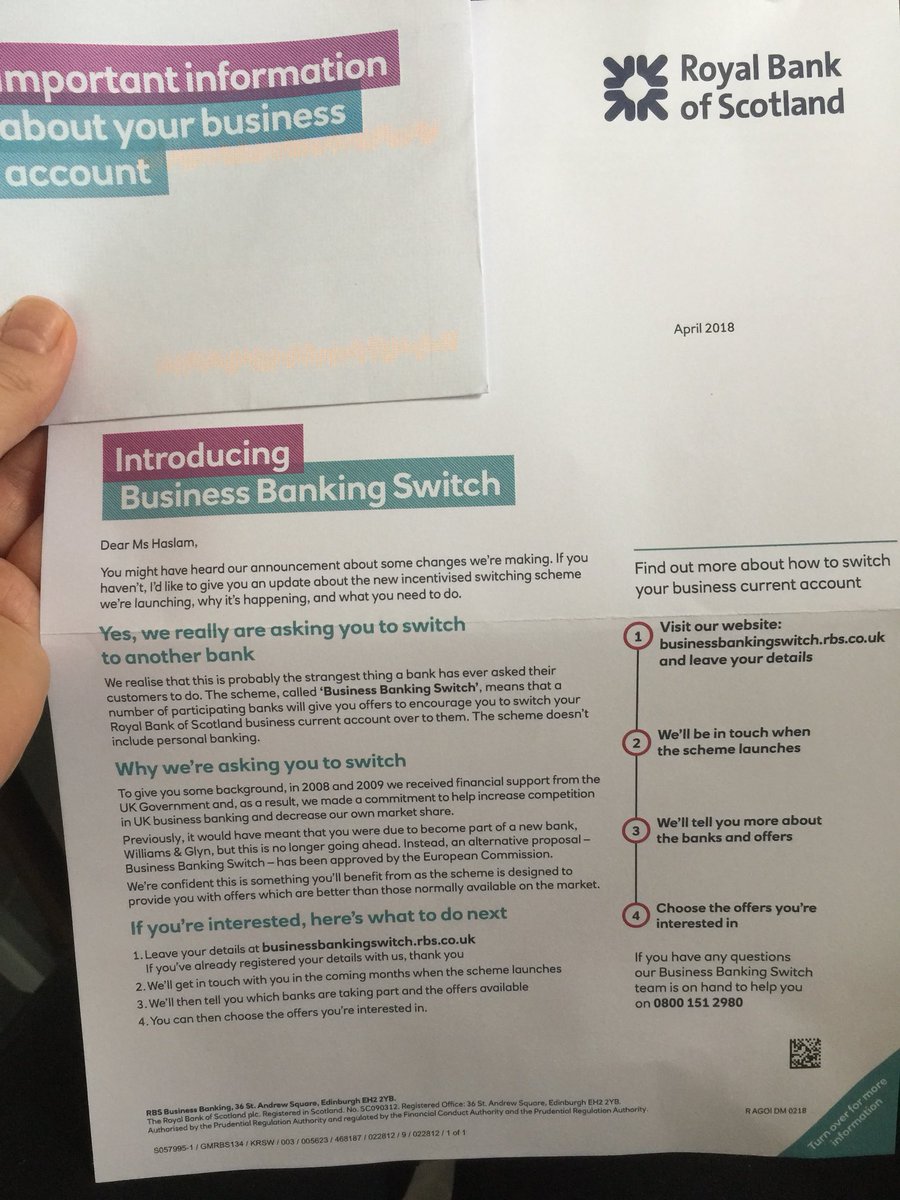

The second part, which affects customers directly, is the #Incentivised Switching Scheme (although it has become known as the #Business Banking Switch scheme). This is a bizarre scheme whereby eligible challenger banks (i.e. smaller competitors) are incentivised to take eligible SME customers from W&G by being paid – by RBS – what is effectively a ‘dowry’ which comes with the account.

A total pot of £225m has been put up by RBS to switch business current accounts – with another £50m to go with loan accounts. Plus there is a budget of £75m to cover the costs to customers of switching, for example if they have to pay for valuations for security or pay early redemption fees. So a total of £350m for RBS to effectively ‘Sell’ their SME customers (incidentally the definition of an SME for this purpose is a turnover of £25m or less)

Only a small number of banks can participate in this and they are going through an Application process. Clydesdale and Santander appear to be ‘front runners’ both wanting to get involved in improving the practicalities of it to ensure that it goes as well as possible

It will be up to the ‘Receiving Banks’ to decide how to apply the ‘dowries’ that they get. Logically they will use a good part to incentivise the client moving by offering them discounts on loans, fees etc, but they are not compelled to.

The process is as follows:

- RBS have 18 months from the opening of the scheme to achieve what they have been set

- RBS have started contacting eligible customers to formally register their interest in switching. These are of course mainly the same customers who had a letter a couple of years ago saying that they were being ‘sold’ and nothing actually then happened – so they may not treat this too seriously. Also many of the letters went out as early as April 2018 – probably forgotten about now?

- A new RBS ‘microsite’ has been built for people to register on – and by 19th December the banks participating will be agreed and announced.

- The website goes live for switching customers on 25th Feb 2019 and it will show them what the offers are from the other banks (a sort of ‘compare the market’ in terms of what incentives are being offered)

The incentives for the current account alone are based on turnover – and are not to be sneezed at – a business with turnover of less than £15k will get £750 but one with turnover of over £7.5m will get £50k – and that is just for the current account. Of course this figure goes to the Receiving Bank and it isn’t known to what extent it will be passed onto the customer.

The dowry for Loan products is calculated as 2.5% of the loan amount. So a loan of say £100k would have a dowry of £2.5k. A £1m loan (not unusual if a property was involved) would be £25k.

There is also provision for ‘Additional Payments’ which will go through an arbitration process – and cover one-off costs such as revaluations and break-costs (up to £10k per customers has been nominated for legal fees and £1,200 for property valuations – although this is unlikely to cover the actual costs of a valuation unless it is a ‘re-write’)

As well as the turnover criteria it will be ruled that any business will be excluded if it is in arrears or ‘in financial difficulty’ (although there appears to be no definition of that)

In total about 217,00 businesses are eligible for this and RBS have to ensure that a minimum of 120,00 business accounts go to ‘eligible challenger banks’.

It is not difficult to see some issues here:

- Firstly the businesses have to register – which they do through a site called www.businessbankingswitch.rbs.co.uk. Unless they register (when they then get a unique reference code) they will not get further details of the scheme when it goes live on 25th

- Switching is not mandatory – they cannot be forced to go – but they will be incentivised to do so

- RBS only get recognition if the business transfers to one of the scheme approved banks – they will inevitably be smaller banks and a good sized company, with complex needs, might prefer to move to another large bank.

- The devil is in the detail – talking to one banker closely involved it seems that they are still tying to get basic questions answered about how this will work in practice – and the timescales are tight (offers will be on the website on 25th Feb and no slippage has been allowed)

- A sudden interest from 200,000 businesses risks swamping a smaller bank. There’s talk of ‘triage’ teams to decide who they deal with first.

- The new bank will be able to do its own risk assessment and decide if it wants the business and, most importantly, how much they are prepared to lend them and on what terms. They may not be able to replicate the RBS package that the client has (although in some cases they may do better)

- Commercial lawyers and property professionals (especially valuers) are already stretched – this could cause a surge in work loads

- Switching banks is very disruptive to businesses – hence the inertia that is always seen

- On-boarding such accounts is demanding – how will the receiving banks cope and get things right

There are opportunities here of course:

- For the receiving banks selected (decisions will be made as to who they are in December) they will have unfettered access to a chunk of businesses who are being encouraged to leave RBS, by RBS, and will have money to incentivise them. They could significantly grow their SME banking book in a way that would otherwise take years.

- The SME’s affected will be financially rewarded

- SME’s could see this as a way of escaping existing deals which might for example have breakage costs

- Professionals such as lawyers will see an increase of work in respect of legal activity

- SME’s should really seek help in assessing other banks schemes and getting support during the assessment and switching process.

Personally, I’m anticipating having to commit time in 2019 to a small number of SME’s who decide early on that they need to get outside help in:

- Making an informed decision on whether to switch or not

- Presenting the best case to a new banker to gain from any improved package that might be available

- Maximising any payments that might be available – the obvious opportunity is for any RBS/W&G businesses that have SWAP or IRHP deals that they would like to get out of but where they can’t afford the breakage costs.

The first piece of advice is to ensure that any eligible businesses must register. It doesn’t commit them to anything but it does mean they are given the option and will be automatically involved in the next stage.