With a third of the MPC having voted for an interest rate rise yesterday (21st June) the prospects of the cost of funds for SME’s rising this year are increasing.

a third of the MPC having voted for an interest rate rise yesterday (21st June) the prospects of the cost of funds for SME’s rising this year are increasing.

An interesting article in ‘Accountancy Age’ last month drew attention to the serious impact that this could have on the UK’s mainstay businesses, with additional costs of £355m (in one year) coming from just an increase in base rate of 0.25%.

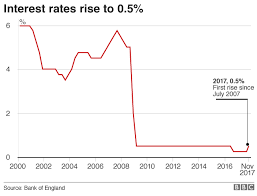

It is difficult for a business owner to relate to this figure but not tricky to work out that with many businesses working on narrowing margins, and many still relatively highly geared, this will be painful. The graph alone illustrates what a unique period we have come through.

It’s a concerning fact that 5 years ago as much as 50% of SME lending was on fixed rates or ‘hedged’ (a form of insurance protection against rate rises) but this is said to have now reduced to 11%. This means that significantly more businesses will bear the costs of this inevitable event.

The reasons for this appear clear:

- It’s human nature to focus more on ‘insurances’ of any kind once an event becomes prevalent – so you put in security cameras and beef up your home insurances only after a spate of burglaries in your road.

- An extraordinary 10 years of static and low interest rates means this has not appeared priority in a business owners in-tray. Indeed, in many cases (given the life-cycle of businesses) many have never known anything else and don’t have painful experiences to recall.

- The scandals associated with the sale of ‘SWAP’s’ (by the main High Street banks) to SME’s has hurt the banks and destroyed the credibility of these products in the eyes of borrowers. Perceptions would make it hard for a bank to promote this option to SME’s where it has been proven to represent a reputation risk to the bank (it remains a credible option for bespoke, high value packages for Corporates with Treasury functions). It would be a bit like a retail bank going back to selling PPI.

- SME’s have very little if any access to advice on this. Trust in the banks will be thin at best, Accountants are not the best to advise on this (the article in their trade magazine seemed like an attempt to just gain their interest) and specialist advisers in this area tend to be ‘City based’ and focus on the legalities of contracts, with perceptions that they are very expensive.

- If there was a shortage of advice ‘Pre-SWAP-gate’ there will be even fewer now – who is going to stick their neck out on this subject?

- Banks recent pricing of fixed rate products hasn’t created the incentive for SME’s to take up a fixed rate, either by alarming them with the bank’s opinion of where rates are going or by offering them an incentive for their perception that locking into a fixed rate could now be seen as a risky venture.

- Most significantly many banks (particularly the recent entrants to SME lending) are not even offering fixed rates. They find it as difficult as any to predict rates and formulate pricing and would prefer not to carry the risk on their own book. Instead they have a policy of lending and giving the client the option to take out a hedging product with a third party.

The impact of this is that SME’s are exposed to the risk themselves and will carry the inevitable costs. This will of course have a knock-on effect on the banks’ risk – they are only as good as their borrowers. So are the banks ‘shooting themselves in the foot’ by not being more bold or assertive in this area? Yet again we have a gap in the market for financial products for SME’s due to policy changes by lenders, which requires a careful approach from, and towards, those that may seek to fill it.